UKRAINIAN DEFENCE TECH MARKET 2024: DataDriven Study

DataDriven has published the Ukrainian Defence Tech Market Report. Defender publishes key details

Key indicators of the Ukrainian defence tech industry

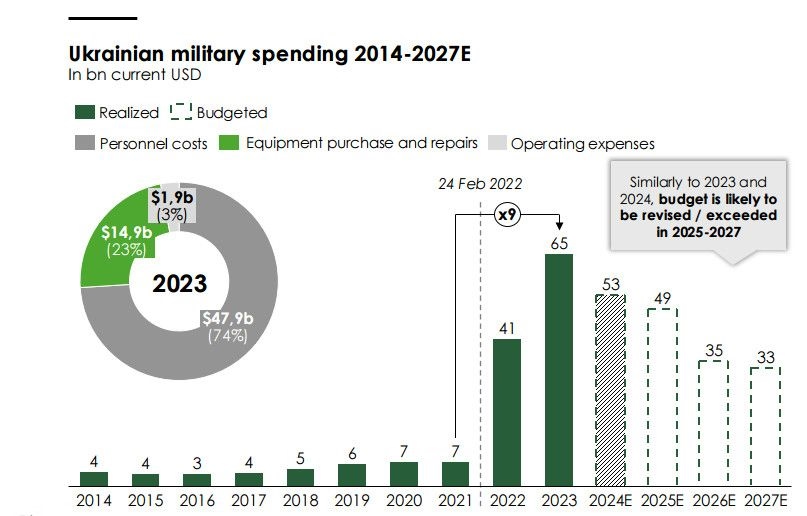

Record military funding. In 2023, Ukraine’s defence spending reached a record $65 bln, nine times more than in 2021. Of this amount, $15 bln was allocated for the purchase of defence equipment. In 2023, military spending accounted for 37% of GDP and 58% of total government spending. In 2024, the initial defence budget was $41 bln, but it was subsequently increased by about 30%, reaching $53 bln in July 2024. Military operations are projected to continue at least until the end of 2025.

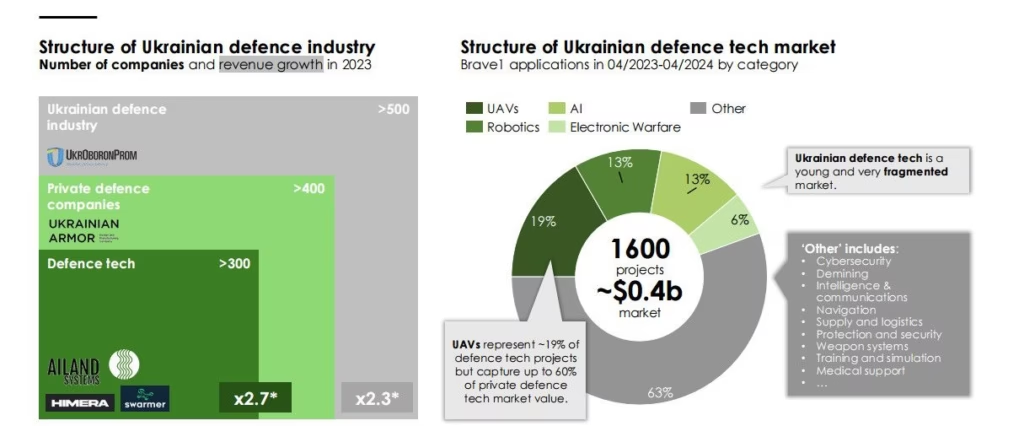

Growth of the domestic defence industry. Ukraine’s defence industry was valued at $3 bln in 2023 and is expected to grow to $5 bln by the end of 2024. This growth is driven by both domestic demand and government initiatives aimed at strengthening the military-industrial complex.

Defence technology market. In 2023, the defence start-up segment in Ukraine more than doubled, reaching approximately $0.4 bln. There are more than 300 companies operating in the market, which indicates a great potential for innovation in this area.

UAVs are the fastest growing sector. Although only 19% of defence technology projects involve drones, they account for about 60% of the total value of Ukrainian startups. In 2023, 96% of public procurement of unmanned aerial vehicles was made from domestic suppliers. In addition, from September to December 2023, the number of strikes carried out by FPV drones increased sharply from 67 to 1,059, an increase of 709%.

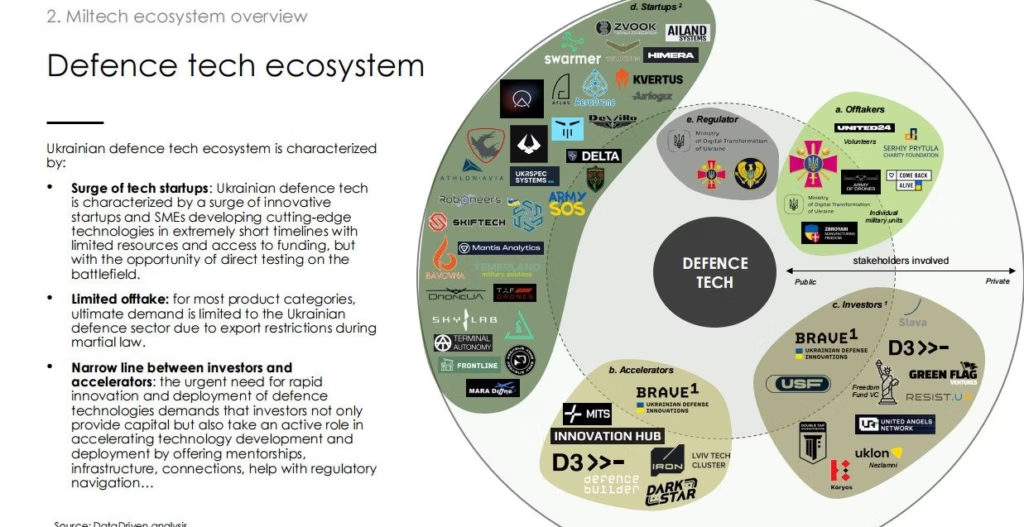

Defence technology ecosystem

- Startup boom. Ukraine’s defence technology ecosystem is witnessing a rapid growth of start-ups, especially in the areas of drones, cyber security and artificial intelligence. These companies are developing cutting-edge solutions with limited resources, benefiting from the ability to test their technologies directly on the battlefield.

- Main users. The Ministry of Defence, volunteer organisations and international donors are the main customers for defence technology. Individual military units also sometimes receive systems through volunteer initiatives.

- Incubators – driving development. Incubators such as Brave1 play a key role in the development of the defence technology ecosystem by providing funding, infrastructure and mentorship. In 2023, Brave1 invested $2.7 mln in defence projects, and plans to invest $39 mln in 2024. The Cluster has tested more than 2,000 defence solutions.

- Defence accelerators. Accelerators facilitate the rapid development of defence technologies by offering not only funding but also infrastructure, advice and assistance in navigating regulatory processes. This gives start-ups the opportunity to scale their solutions and get to market faster.

- Funds invest in miltech. New investment funds are being created in Ukraine, such as Freedom Fund VC and Uklon Nezlamni, which focus on financing defence technology start-ups. Traditional venture capital funds are also willing to support promising developments, which significantly improves access to capital for start-ups.

Who invests in defence start-ups and how

- Specialised funds. Funds such as Freedom Fund VC focus on sectors with high growth potential, such as drones, artificial intelligence and cybersecurity. Investors are looking for technologies that can be quickly scaled up for military and civilian use.

- The role of universal funds. An increasing number of generalist funds are starting to invest in defence technologies, motivated by the high return potential and strategic importance of dual-use technologies.

- Who they invest in. Investors focus on solutions that can quickly enter international markets. This avoids dependence on domestic demand in Ukraine, which may decline after the war ends.

- Investor restraint. Many funds avoid investing in defence technology due to the complexity of the sector, high risks and specific regulatory requirements. They prefer more mature markets, which affects the pace of capital raising in this sector.

- Patriotic investments. Some investors are driven by patriotic motives, prioritising support for Ukraine’s defence capabilities, even if it does not bring immediate financial benefits.

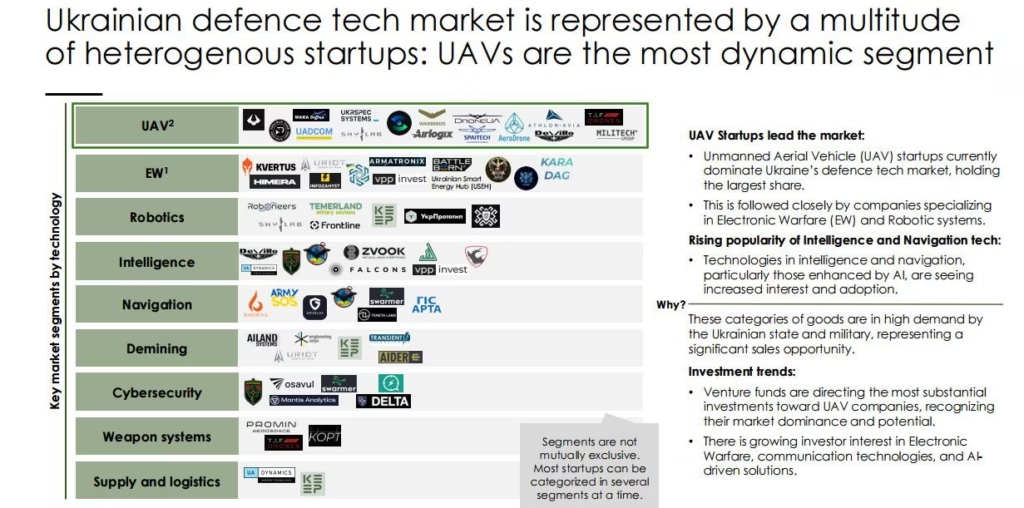

What areas are being developed by Ukrainian start-ups

- UAVs startups hold the largest share of the Ukrainian defence technology market and attract the most investments. This indicates a high development potential in this segment.

- Electronic warfare, robotics, intelligence. Other major technology segments that are actively developing include electronic warfare, robotics and intelligence technologies. These areas are also attracting investor attention and show significant potential.

- Trend towards dual use of technology. Investors are actively supporting start-ups that develop technologies that can be used for both military and civilian purposes. This increases the attractiveness of such companies in the market and expands their potential market. Among the startups worthy of attention are:

- AiLand Systems specialise in drones for mine clearance.

- Himera develops radios and radio systems for military and rescue services.

- Buntar Aerospace focuses on reconnaissance drones using AI.

Regulatory policy and key challenges

- National Defence Procurement Agency. Since 2024, all procurement for the Ministry of Defence of Ukraine has been carried out only through the National Defence Procurement Agency. This ensures a centralised procurement system, increasing transparency and efficiency of processes.

- Simplification of procurement for UAVs. The procurement procedure for drones has been simplified by cancelling VAT and customs duties on the import of drones and their components. This innovation accelerates the development of the UAV industry in Ukraine.

- Export restrictions. Since 2022, Ukraine has been subject to restrictions on the export of military and dual-use goods, which significantly limits the ability of Ukrainian companies to enter international markets. This has a negative impact on attracting investment, as the state does not have sufficient funds to contract 100% of available products.

- Product certification. All high-tech military developments must be certified by the Ministry of Defence. The certification process involves testing of products to ensure that they meet standards. While this procedure could previously take several years, efforts are underway to de-bureaucratise it, leading to faster certification.

The full report is available here.

Reading now

1

Ukrainian SkyFall’s drone wins at Pentagon’s Drone Dominance selection

2

Black Forest Systems raises $400,000. Here’s what drones the startup is building

3

Sting interceptor by Wild Hornets downs costly Russian Granat-4 reconnaissance drone

4

UForce unveils Bucha middle-strike drone with a 200 km range

5

The F10 drone becomes the second Ukrainian finalist in the Pentagon’s Drone Dominance Program

By submitting this form, you give Defender Media consent to the processing of personal data.

Надсилаючи цю форму, ви надаєте Defender Media згоду на обробку персональних даних.

Latest insights

1

What defence manufacturers need to know about Defence City — insights from the UCDI’s Head of GR

2

“In a year, my unit destroyed over 3,000 aerial targets.” Maksym Zaichenko on the 3rd Army Corps air defence system

3

Intelligence dependence as a strategic vulnerability: From satellite constraints to autonomous analytical platforms

4

A full-cycle unmanned business: Drone Fight Club founder Vladyslav Plaksin on manufacturing, pilot training, and investment

5